Articles

| Name | Author | |

|---|---|---|

| Case Study: Singapore Lessor (DAC) Eyes Further Digitalization | Jefferson Ding, Managing Director at Dragon Aviation Capital (DAC) | View article |

| Case Study: Engineer Training and Monitoring Solution Project at FL Technics | Liudas Jurkonis, Deputy CEO for Engineering, Design and Technical Training Department, FL Technics | View article |

| White Paper: IT systems adoption Part 3 | Allan Bachan, VP, Managing Director, MRO Operations, ICF | View article |

| WHITE PAPER: Sustaining aviation after recovery – part 2 | Gesine Varfis, Marketing Manager APSYS and Gabriel Godfrey, Product Owner – Sustainable Aircraft, APSYS | View article |

WHITE PAPER: Sustaining aviation after recovery – part 2

Author: Gesine Varfis, Marketing Manager APSYS and Gabriel Godfrey, Product Owner – Sustainable Aircraft, APSYS

Subscribe

Gesine Varfis, Marketing Manager APSYS and Gabriel Godfrey, Product Owner – Sustainable Aircraft, APSYS explain why the aviation recovery will be digital – sustainable and green

In part one, we looked at the challenges that commercial aviation faces today and will still face after the pandemic has passed; how different parts of commercial aviation might be differently affected and a first look into the future for the sector. In this part, we’ll look further into the future and, in particular, at some new ways of working that are already in play or that could be introduced in the years ahead. We’ll look at how the sector can play its part in dealing with climate change.

STATUS, IDEAS AND APPROACHES

Aerospace and Aviation have a long track record in sustainability. British Airways, KLM and Lufthansa have been publishing corporate sustainability reports since the 1990s. At the same time aerospace manufacturers have been designing increasingly fuel-efficient aircraft. According to ATAG (Air Transport Action Group) today’s jet aircraft are well over 80% more fuel efficient per seat kilometer compared to the 1960s, and the new Airbus A350 and A220, Boeing 787, ATR-600 and Embraer E2 aircraft use less than 3 liters of jet fuel per 100 passenger kilometers. This matches the efficiency of most modern compact cars.

In parallel, significant efforts have been made to decrease the consumption of fossil fuels in ground handling and aircraft operations. Paperless operations from e-ticketing (2009), IATA Guidance Material for Paperless Aircraft Operations in Technical Operations (2017) and other digital initiatives have been launched. ATM optimization projects such as SESAR (Single European Sky ATM Research) are making taxi-out times more predictable and efficient, allow the reduction of holding patterns, vectoring in terminal airspace upon arrival and optimizing trajectories through the use of i4D, among other technologies.

Despite these efforts and achievements, traffic growth has off-set all of these savings, making it clear that any path to net-zero-emissions requires radical technical and operational changes and innovations. Such drastic evolutions are only possible if they are driven by stimuli and enablers.

During the 1973 Middle-Eastern oil crisis fuel became one of the top cost drivers. The prediction was that fuel would become more and more expensive, making fuel-efficient aircraft, fuel efficient operations and fuel hedging vital competitive advantages. Investments into aircraft R&D ramped up and led to the spectacular improvements listed above. Later, in 2004, IATA launched its fuel efficiency program in response to the further rising price of fuel, supporting airlines to increase their fuel efficiency and reduce CO2 emissions. Weight reduction programs and alternative fuels have gained traction ever since. Finally, governments have been driving old aircraft out by laws or regulations, or enforcing carbon off-setting programs onto airlines.

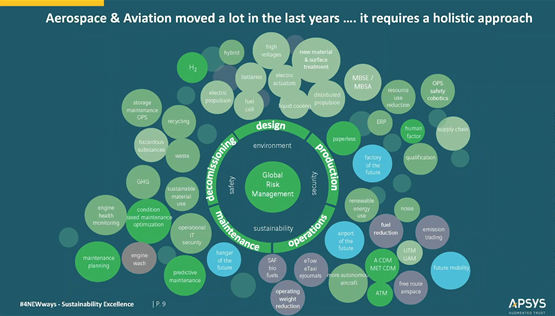

Until now the low hanging fruits have been identified and many carriers have harvested them. The continued improvement of existing initiatives and the deployment of new, radical solutions (figure 4) will only be effective if they are introduced with a cradle-to-cradle or circular approach. For efficient tradeoff, the impacts – including environmental – of initiatives of all types and scope must to be simulated, predicted and monitored throughout the whole aircraft lifecycle including design, materials sourcing, factory of the future production, future airport and flight operations embedded into future mobility concepts, and hangar of the future maintenance – driven by condition-based maintenance, decommissioning and recycling.

This holistic cradle-to-cradle environmental traceability will rely on new tools and new ways of working, more data collection and analytics to enable business resilience as well as failure and disruption mitigation. Last but not least it will require joint efforts and a level of consensus over all ecosystems from business and stakeholders to society in general, governments and consumers.

TODAY’S EFFORTS, ALTHOUGH HARD TO ACKNOWLEDGE, ARE NOT GOOD ENOUGH

The green premiums concept introduced by Bill Gates as an enabler of achieving zero-emissions relates to the additional cost of choosing renewable energies or a clean technology over one that emits a greater amount of greenhouse gases. For jet aviation fuel Gates estimates a 140 percent increase based on an average jet fuel price of $2.22 per gallon. If this materializes it will have a massive impact on travel behavior. Therefore, we need to find ways to make green premiums cheaper.

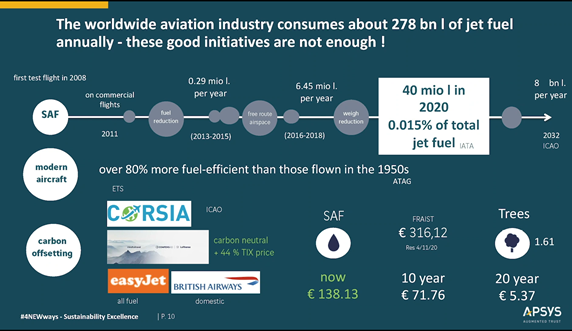

The worldwide aviation industry consumes about 278bn liters of jet fuel annually (figure 5). This is the amount of fuel to be reduced and/or compensated to achieve net-zero emission without taking future growth into account.

One of the most prominent actions to reduce carbon emissions is the use of Sustainable Aviation Fuels (SAF). The first test flight with SAF was in 2008 and the first commercial flight in 2011. However, SAF represented just 0.015 percent of total fuel consumed by the industry in 2020, while ICAO has predicted that 8bn liters of fuel per year can be produced in a bio-environmental manner by 2032. This is a drop of water on a hot stone.

One of the other important actions taken are off-setting programs like CORSIA. However, as customer focus on CO2 has steadily and constantly increased, airlines have initiated their own programs for offsetting CO2 emissions. Delta announced plans to invest 1 billion USD over the next decade in offsetting initiatives, like SAF and carbon sequestration. Carriers like EasyJet offset all their fuel consumption, while British Airways offsets domestic flights leaving it to customer’s choice for offsetting on all other routes.

Lufthansa has moved the complete off-setting initiative to its customers. How that works is that, for a trip from Frankfurt to Istanbul, the fare was €316,12 on November 4th 2020. Customers had the choice between planting trees and offsetting their carbon emissions over twenty years for about €5 or over ten years for about €70. For comparison, the price for offsetting the trip with biofuels would represent a 44 percent increase of the ticket price (+€138,13). When taking the range of 44-140 percent increase into account it becomes clear that aviation needs to get prepared for managing a very uncertain future.

Today SAF can be blended with traditional jet fuel up to 50%. With 14% of customers, according the World Economic Forum study, willing to pay higher premiums voluntarily there is room for improvement. Even when we are able to achieve, that on all flights worldwide, even with 50% of SAF on board it will not be good enough to meet the goal of net zero-emissions. As of today, aircraft and engine manufacturers are working hard to develop aircraft that can be fueled with 100% SAF.

This brings us to the question of who needs to drive aviation sustainability and how we can assure, within a highly price-sensitive industry, that airlines do not lose passengers to a non-offsetting competitor because of the high premiums set.

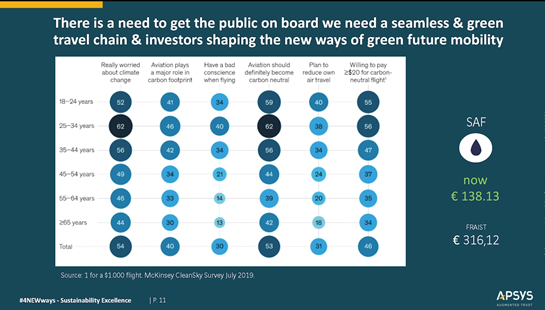

McKinsey performed a survey in 2019 (figure 6) which reveals a generation gap with the younger generation being more concerned about climate change compared to other age groups. Those in the age group of 25 – 34 have the strongest position on climate related issues, but are generally not willing to change their travel behavior. Above 45 years, people are less sensitive to these issues. Throughout all age groups the worry about climate change is ranked higher than the willingness to pay a green premium even considering the fact that the proposed price increase is far from the cost of net-zero flight: in the previous example of the flight from Frankfurt to Istanbul the SAF green premium was a +44 % price increase. This survey proposed an offset price of only US$20 for a US$1,000 flight which translates into a 2% increase.

This survey highlights the fact that a green recovery requires not only a radical change in technology. Society needs to change attitude and commitment towards sustainability, it requires an active engagement and contribution by everyone. Changing customer habits is a very sensitive undertaking. It requires strong change management, a very much closer customer relation, as well as risk management capabilities which take account of much more than environmental risks. This makes a green recovery an extremely uncertain, complex and critical challenge, especially since we can’t wait until a new zero-emission aircraft is ready to operate commercially. It requires more than just shareholder value focus; it requires trust and collaboration in rebuilding and re-engineering the future together. Therefore, we might even take the more personalized and individualized services into a new area of C2B relation management based on very close interaction with customers to reduce risks to a minimum.

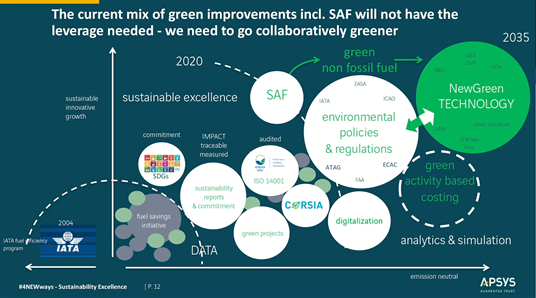

Looking at what has been achieved and what it takes (figure 7) to achieve zero-emission travel. There is still room for taking the current initiatives like CORSIA and SESAR further and getting everyone on board for the Sustainable Development Goals (SDGs) to achieve sustainable excellence. This will be the next obvious steps. For this and what is ahead of us, we need to work closely with regulators and institutions which will help us to define the framework and ensure compliance. Transparency will also be necessary to build customers’ trust into the efforts taken. We need stronger tangible goals on the road to zero emission for 2050.

TRANSFORMATION TO NEW CAPABILITIES AND TECHNOLOGIES

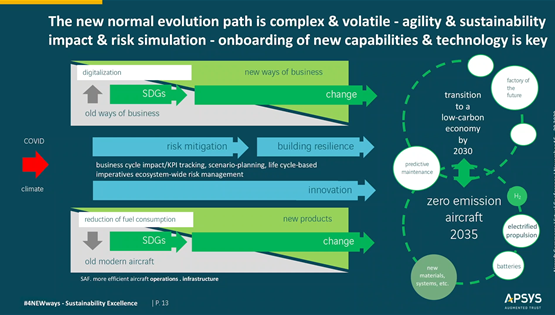

As important as operational excellence has become, achieving net zero-emissions requires the introduction of the concept of sustainable excellence and how we intend to achieve it (figure 8). The path towards this ideal is complex, uncertain and volatile. New tools to manage this transformation will be necessary.

In the coming years, the modern fuel-efficient aircraft of today will be further improved. In parallel, radically new aircraft concepts will be developed and introduced. Both processes will have to be managed and synchronized by all industry stakeholders worldwide. One of the enablers for managing this undertaking is the power of big data and advanced analytics tools. Analytics, predictive and prescriptive analytics and simulation make complexity and future uncertainty manageable. Agile development efforts combined with digitalization and risk management will ensure business resilience, while environmental impact and scenario planning will maximize the efficiency and limit the impact of the introduction of new technologies.

The new normal in aviation will be a lot different from what we know today. Over the last two decades we have talked about EFB in the cockpit and paperless maintenance and whoever has been involved in electronic signature approval knows what it takes to get only this approved with the authorities. Safety comes first and always will, however, proven as well as new technologies need to be adopted faster and by everyone to achieve zero emission.

The areas of new technology fast-tracking go beyond aircraft design and fuel. A circular economy approach is vital in all areas, not only the ones related to customer experience. ROI (return on investment) will be defined differently taking sustainability impact into account. The ‘behind the scenes’ aircraft maintenance will be one of the domains with significant environmental leverage beyond today’s ISO14001 framework in respect to materials, paint, waste, smarter re-use and recycling. Last but not least the days of the traditional letter checks are numbered; MPDs (Maintenance Planning Documents) support individualized, equalized checks while the industry and beyond work on condition-based maintenance concepts based on predictive maintenance.

In the future, we’ll need to be very much more agile and look at sustainability as a risk and opportunity. We need to simulate the impact of the risks and the new ways of working, to understand the outcomes while staying open-minded for alternatives. Complementary collaboration is a good way of reducing uncertainty and risks.

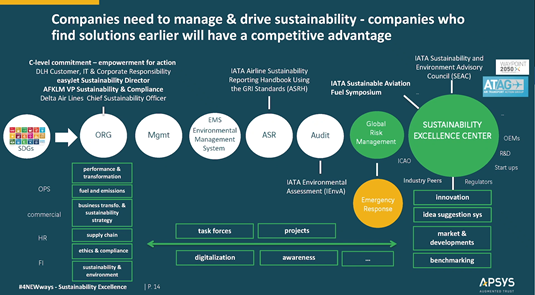

The framework for managing the new ways of doing business

Like Operational Excellence, Sustainability Excellence will only have an impact if it is entrenched into daily work and operations. In figure 9 we can see what regulations, tools and processes are currently deployed by many companies.

The UN Sustainable Development Goals (SDGs) are an accepted standard to define comparable goals, missions and visions. Translating this vision into action requires shared goals, a strategy and an adequate organizational structure with sponsors or responsibilities assigned within the organization. Some companies have already been implementing this as sustainability has gained C-level attention throughout the industry: Lufthansa has a Chief Customer Officer responsible for Customers, IT and Corporate Responsibility; EasyJet a Sustainability Director; AirFranceKLM a VP for Sustainability and Compliance; Delta Airlines a Chief Sustainability Officer. This demonstrates the prominent role that sustainability already plays.

Incorporating sustainability into the management process requires an environmental management system (EMS). It’s comparable to what we know from IOSA (IATA Operational Safety Audit) and its safety management systems (SMS). Like the SMS the EMS requires auditing; reporting as well as traceable continuous improvement. IATA has published an Airline Sustainability Reporting Handbook with guidelines as well as the IATA Environmental Assessment (IEnvA) program specifically developed for the airline sector. IATA offers consulting, has established a sustainability innovation forum as well as the Sustainability and Environment Advisory Council (SEAC) with twenty airline members.

Similarly to SMS, EMS includes the raising awareness and continuous improvement related to sustainability. Other industries have established line functions or ‘Sustainability Excellence Centers’ responsible for driving sustainability projects and innovations while including suggestion systems, market development follow up and benchmarking. For EMS reporting and auditing there are numerous tools available in the market, but for managing sustainability continuously more is required.

A NEW WAY FOR ENVIRONMENTAL COMPLIANCE WITH BPM?

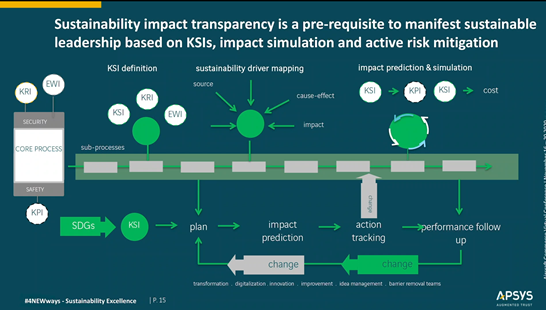

Tools in use today are focused on action management and sustainability monitoring for CSR and EHS initiatives embedded into an audited sustainability reporting. With environmental compliance getting more complex, with requirements changing at faster pace, the need to assure compliance with software tools to avoid penalties or impact on trust into the brand rises. Many companies treat compliance and business process management (BPM) separately, but with environmental impact and CO2 emissions being related to all business processes, BPM could move into focus for compliance assurance, transparency, risk management and impact simulation. This will require more detailed data about the sources, cause/effect relations and impacts via a sustainability and CO2 impact driver mapping (figure 10).

To feed these indicators, data collection must evolve from basic quantity measurements (for example a simple metric of waste produced annually) to a detailed data relations mapping over the complete business process (from source to disposal or recycling) related to key performance (KPI), key risk (KRI), key sustainability indicators (KSI) and cost. In addition, early warning indicators (EWI) allow proactive management of deviations in real time before they have a significant impact. If changes in cause-and-effect relations can be identified early, they can be monitored and controlled.

This approach represents a new perspective on environmental management and it is too early to say how effective it will be. However, business process management (BPM) tools have a proven impact in increasing productivity, in reduction of cost and cycle times while ensuring quality improvements.

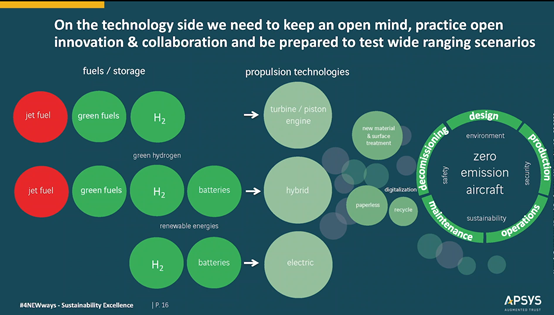

WHAT DOES IT TAKE? THE GREEN REVOLUTION INITIATIVES We are in the midst of the 4th industrial revolution sparked by the need for an energy revolution to limit climate change. As discussed above, we know that while existing initiative (SAF, incremental efficiency improvements, etc.) are an important step in the right direction, they will not be enough to achieve net zero-emissions. Deploying the more radical innovations that will be necessary to achieve this goal will only be possible with increased transparency, trust and collaboration within and beyond the aviation and aerospace industry (figure 11).

While industry actors engage in massive efforts to develop groundbreaking technologies, the scale of the challenge is such that we cannot expect these to be deployed on a wide scale in the very short term. According to Shell, ‘the effective application of low carbon technologies, such as electric and hydrogen propulsion are unlikely to be in widespread use until 2040 or later’’[1]. Even beyond that, it is very unlikely that a silver bullet technology will emerge as a universal solution similar to what Jet Fuel has been in the past decades.

This means that the industry will have to reinvent itself and accommodate multiple evolving solutions tailored to specific air mobility needs. SAF, Hydrogen, Electric and Hybrid technologies are all likely to support parts of the solution but no one knows exactly how this will materialize.

Adapting to this new, constantly evolving reality will require flexibility, open mindedness and collaboration across the industry. This brings significant risk and uncertainty but with the help of the right sustainability management methodologies and tools, the industry has an unprecedented opportunity to introduce groundbreaking change.

Ends…

Contributor’s Details

Gesine Varfis

At APSYS Gesine is responsible for Airline and MRO Marketing including customer relations, ensuring the digital transformation in close cooperation with clients. Gesine worked as CIO and COO advisor for Aeroflot Russian Airlines engaged in the upgrading of Aeroflot’s OPS systems. Prior to Aeroflot she was a Management Consultant for Lufthansa Consulting focusing on cost cutting, operational excellence, performance management, Operations Control and Hub Control Center re-engineering and IT speciation, verification and implementation projects.

Gabriel Godfrey

APSYS

APSYS is specialized in value creation through technical, human and operational risks control. It offers innovative consulting and software solutions with a high level scientific and technological integration. Designing even more reliable aircraft, securing autonomous vehicles, anticipating the nuclear installation obsolescence or protecting industrial assets against cyber-attacks are the challenges for which APSYS employees’ expertise contributes on a daily basis.

Comments (0)

There are currently no comments about this article.

To post a comment, please login or subscribe.