Articles

| Name | Author |

|---|

Aircraft IT 2022 Survey on Optimization Platforms and new IT Technologies

Author: John Hancock, Editor, Aircraft IT

Subscribe

A powerful insight into how the aviation sector’s plans with regard to IT have developed during the past years of pandemic.

We last surveyed the aviation sector in 2019: a lot has happened since then. The obvious factor will have been the COVID pandemic. Although for airlines and operators, COVID itself is already becoming yesterday’s news, its long-term impact is only just beginning to be apparent. And not least in the changing place of IT adoption and the priorities of the aviation sector. Whereas, previous surveys had shown a continuing but linear rate of progress for IT in the sector, our latest Aircraft IT survey, sponsored by and conducted in late 2021 by Alton Aviation Consultancy, suggests a much larger step change not so much in attitudes to IT but in the roles which IT is expected to fill in the sector’s future and the depth to which it will penetrate every aspect of aviation processes and culture. Let’s take a look at the main points covered in the survey and the findings; plus, some hints at what they might mean for the sector.

THE SURVEY

There were 112 respondents to the survey and, of those, 79 were from airlines (figure 1).

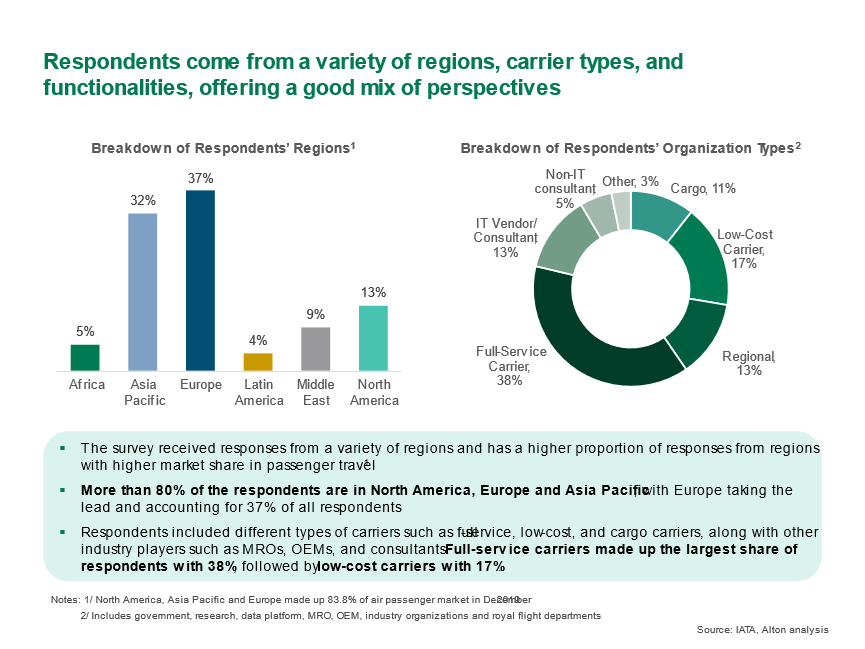

Responses by regions and organization types

Responses to the survey came from a variety of regions but with a larger proportion of responses from regions with higher market share in passenger travel (figure 2).

North America, Asia Pacific and Europe made up 83.8% of air passenger market in December 2019 which is reflected in to fact that more than 80% of respondents are in those regions, with Europe taking the lead and accounting for 37% of all respondents. Respondents also included different types of carriers such as full-service, low-cost, and cargo carriers, along with other industry players such as MROs, OEMs, and consultants. Full-service carriers made up the largest share of respondents with 38%, followed by low-cost carriers with 17%.

SUSTAINABILITY AND OPTIMIZATION IN A POST-COVID WORLD – INTENTIONS AND CHALLENGES

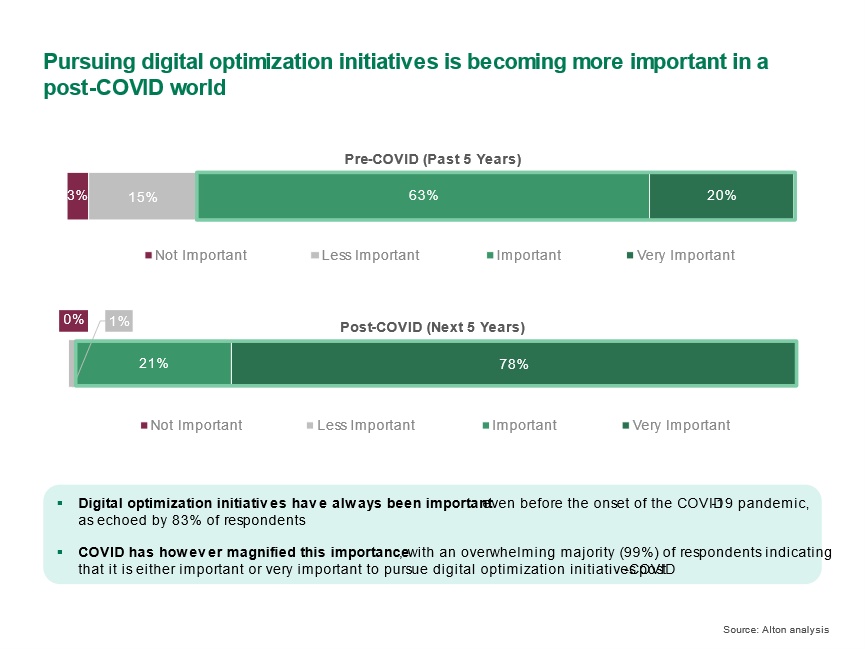

It is, perhaps, no surprise that 99% of respondents indicated that it is either important or very important to pursue digital optimization initiatives post-COVID to manage costs and improve productivity (Figure 3).

Digital optimization initiatives have always been important even before the onset of the COVID-19 pandemic, as echoed by 83% of respondents. COVID has however magnified this importance, with an overwhelming majority (99%) of respondents indicating that it is either important or very important to pursue digital optimization initiatives post-COVID.

Drivers of digital optimization

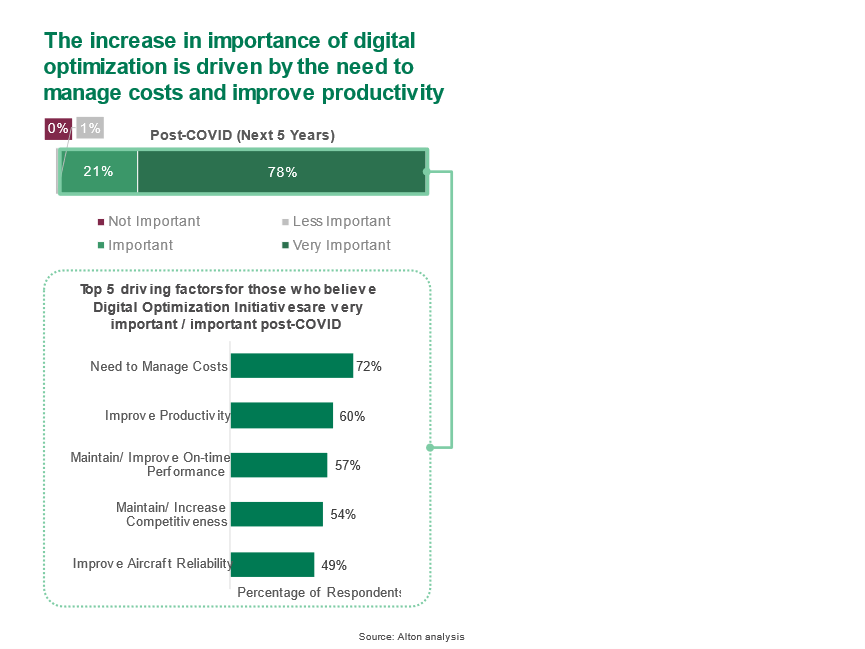

When asked what is driving them along this path to digital optimization, there were five top factors cited by the 99% of respondents who believe that digital optimization initiatives are either very important or important in the post-COVID environment (Figure 4).

The need to manage costs is deemed the most important (72% of respondents) while improving productivity and on-time performance (60% and 57% of respondents respectively) are the next most important factors. Just two of the many comments made by respondents on this were: “Constraints on budget was the biggest push factor. Interest in digital transformation was a means to reduce costs throughout the airline”, and, “With COVID, it is important for any optimizers to be agile and flexible enough to cope with the frequent changes in operations that are a norm today”.

Cost and productivity are never far from the top of any business’s agenda but, with the huge and rapid process changes demanded in order to conduct business in a post-COVID world, those priorities have been amplified and those items on the agenda now have to be in bold capitals. It is encouraging to see how clear is the sector’s understanding on this.

Environment, Social and Governance (ESG) considerations

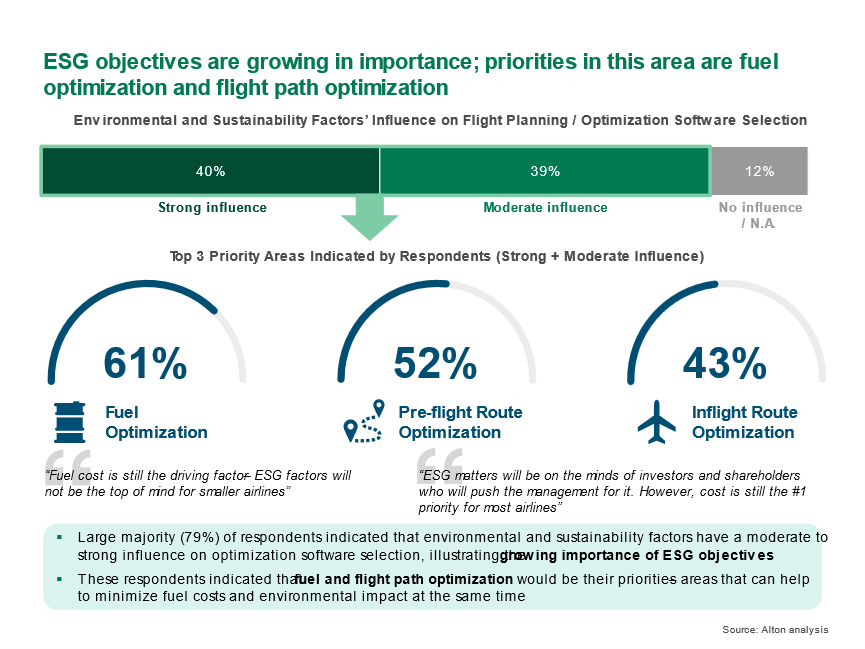

But there are broader factors that have driven the choices that airlines make to realize these trends. Given the high public profile of climate change, that 79% of respondents indicated that environmental and sustainability factors have a moderate to strong influence on optimization software selection, is to be expected. Similarly, fuel and flight path optimization have emerged as key priorities in achieving sustainability goals (figure 5). None of the choices that people make today will be stand-alone, they will all be linked together in the effect.

Although ESG factors are very important and are growing in importance, in the immediate business environment and especially for smaller airlines, it is the cost issues that matter most. However, the effect of tackling those cost issues will also drive sustainability goals.

[[INSERT SLIDE 9 OF Aircraft IT Ops v11 i1 2022 OPS SURVEY (1)Slides with John edits.pptx HERE]]

The challenges

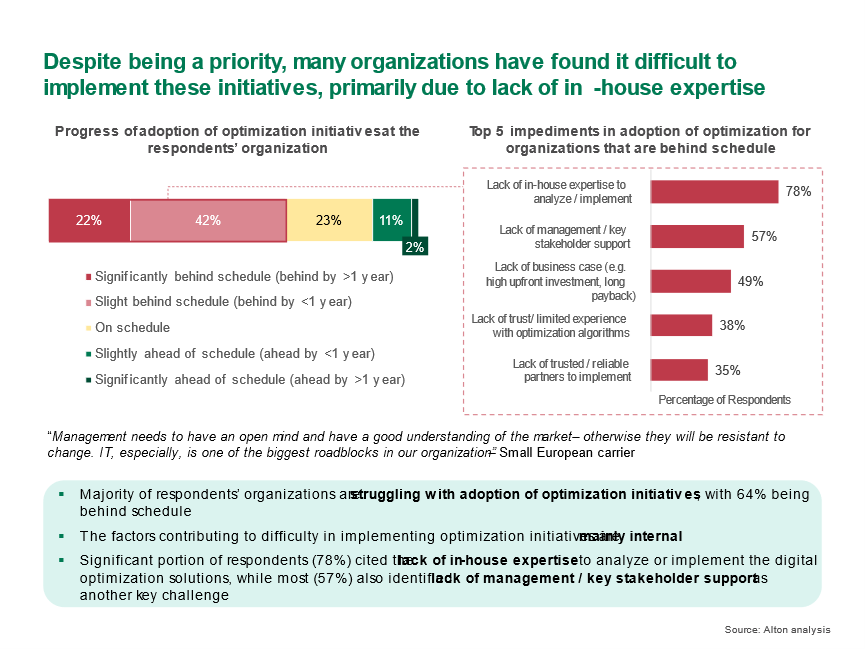

However, ambitious and laudable as these objectives might be, those airlines who responded to the survey were realistic about the challenges that they might encounter when tackling them. When asked what obstacles might be in the way of their achievement of these objectives, 78% of organizations who are behind schedule in adoption of optimization initiatives cited a lack of in-house expertise as one of their top impediments; furthermore, 80% of respondents who felt that optimization projects did not meet expectations cited the same reason (figure 6).

Figure 6

As the figure shows, the majority of respondents’ organizations are struggling with adoption of optimization initiatives, with 64% being behind schedule and, within that figure, 22% being more than one year behind schedule. The factors contributing to difficulty in implementing optimization initiatives are mainly internal. A significant portion of respondents (78%) cited the lack of in-house expertise to analyze or implement the digital optimization solutions, while most (57%) also identified lack of management / key stakeholder support as another key challenge. Some of that lack of support must be linked to the third most cited reason of the initiatives lacking a business case because of high upfront investment but a long payback period. Also, perhaps something for developers and vendors to think about, just over a third of respondents cited a lack of trusted and reliable partners with whom to implement optimization.

The priorities

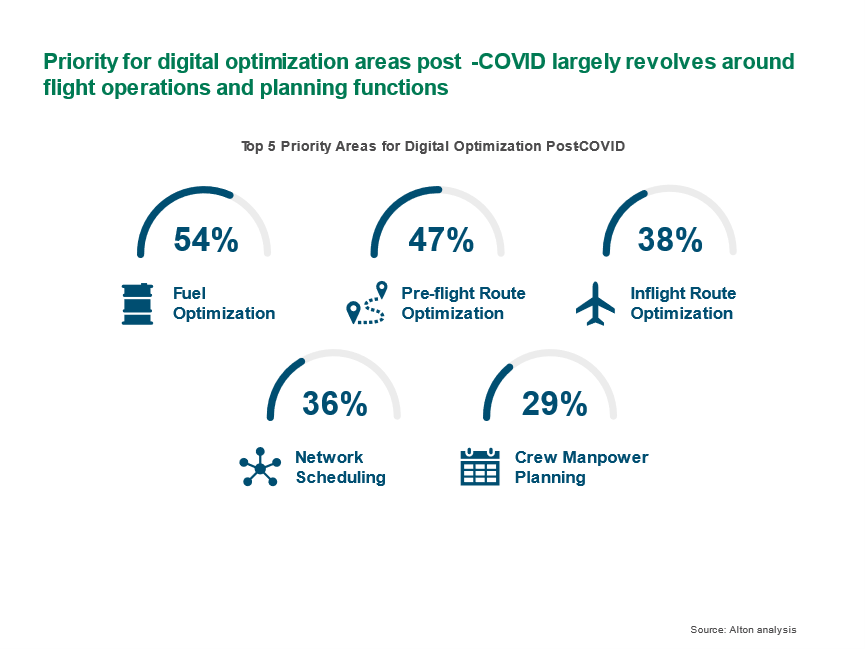

An important element in any adoption of technology or IT based solution is to settle on an order in which to implement things and that means agreeing the business’s priorities. The priority for digital optimization areas post-COVID largely revolves around flight operations and planning functions with the top five priority areas for digital optimization post-COVID shown in figure 7.

Figure 7

As fuel is the largest cost category for airlines, it is unsurprising that fuel optimization was most frequently ranked among respondents’ top five priorities post-COVID (54% of respondents), with a fifth of respondents indicating it as their top priority overall. However, there were other high-priority areas involving flight path optimization, network scheduling, and crew planning. As is the case with many of these findings, it is all about efficiency, productivity and, of course, safety.

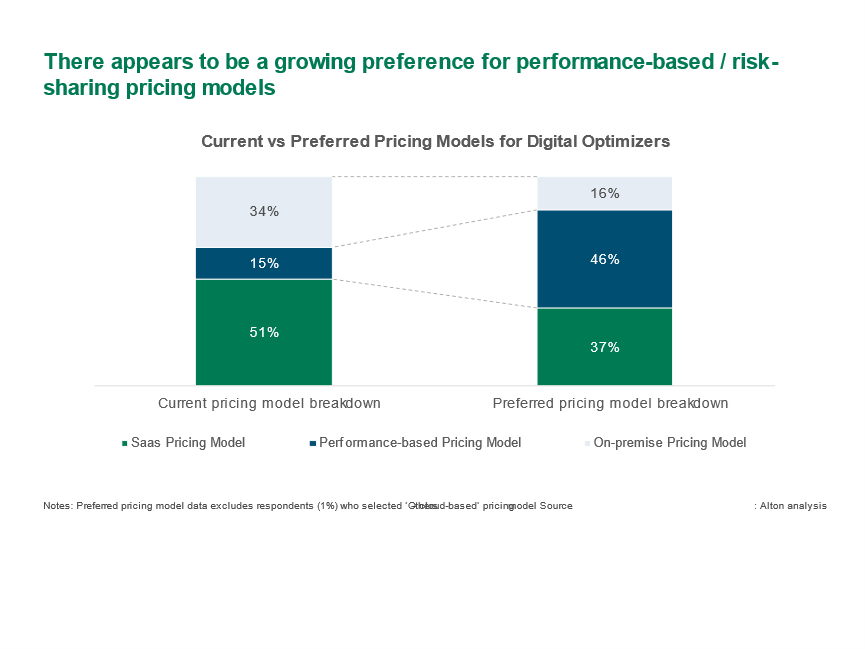

Preferred pricing models: changing preferences

Looking at the survey results, there appears to be a growing preference for performance-based / risk-sharing pricing models (figure 8).

Although today, the SaaS (Software as a Service) pricing model is the most common (51% of respondents) while the performance-based pricing model is the least common (15% of respondents), moving forward, the performance-based pricing model is the most preferred (46% of respondents), overtaking the SaaS pricing model (37% of respondents). Few respondents prefer the on-premise pricing model which entails additional hardware on top of software and recurring costs. Those changing preferences perhaps reflect the ‘Lack of business case…’ impediment in figure 6. Performance-based pricing mitigates the risk in an investment.

Preferred vendors

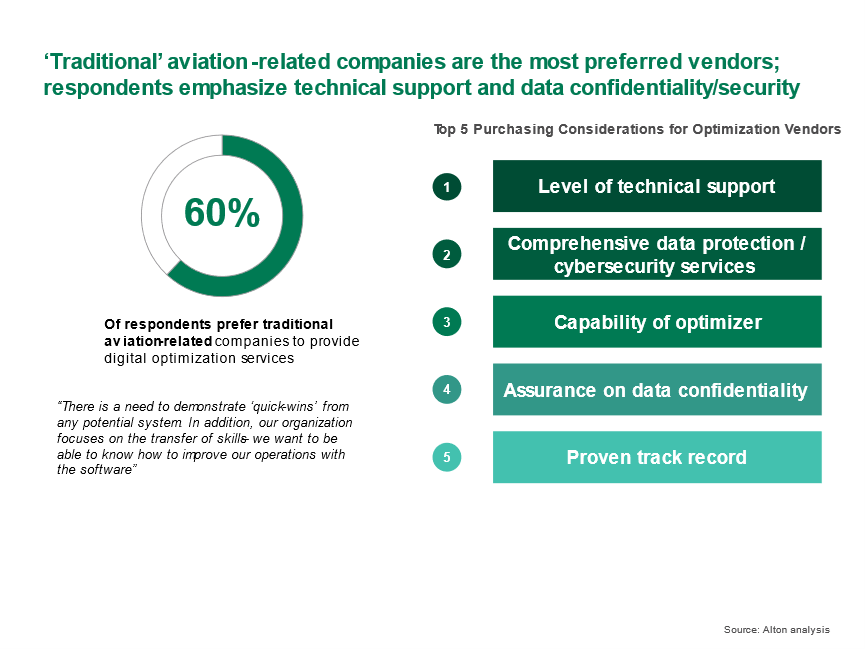

As we know from the many case studies that have been published in Aircraft IT over the years, the relationship between a solution vendor and the buyer/user is a long-term one that requires high levels of trust if it is to succeed. But, as well as that, it also requires a number of other attributes on the vendor’s part for an airline to select them. The survey asked what purchasing considerations were taken into account when selecting an optimization vendor. The responses showed that ‘traditional’ aviation-related companies are the most preferred vendors, with respondents emphasizing the importance of technical support and data confidentiality/security in their procurement decisions (figure 9).

It shows that, for provision of digital optimization services, the majority (60% of respondents) prefer to partner with companies that have traditionally played in the aviation software space instead of alternatives such as data science specialists or technology companies. The top purchasing consideration is the level of technical support, followed by data protection/security and optimizer capabilities. Additionally, as we’ve seen in previous surveys and in case studies in Aircraft IT, airlines are looking for a high level of technical support that runs right through the lifecycle of a solution. Concerns about levels of in-house expertise (figure 6) don’t just determine the speed of adoption for optimization but also, because it’s a long-term commitment, customers need to be confident that support will be always there and will be fast. The fact that ‘Comprehensive data protection/cybersecurity services is the second consideration when choosing a vendor reflects both the growing importance of and potential for vulnerability of IT solutions.

NEW IT TECHNOLOGIES

As well as the traditional technologies of the PC or terminal on every desk, there are a growing inventory of new technologies harnessing not only developments in electronics but also process and application progress. Whereas once, being a year of two behind the latest technology might not have been critical, because IT is so central to modern business, being behind in technology developments can today be a market differentiator.

The Cloud

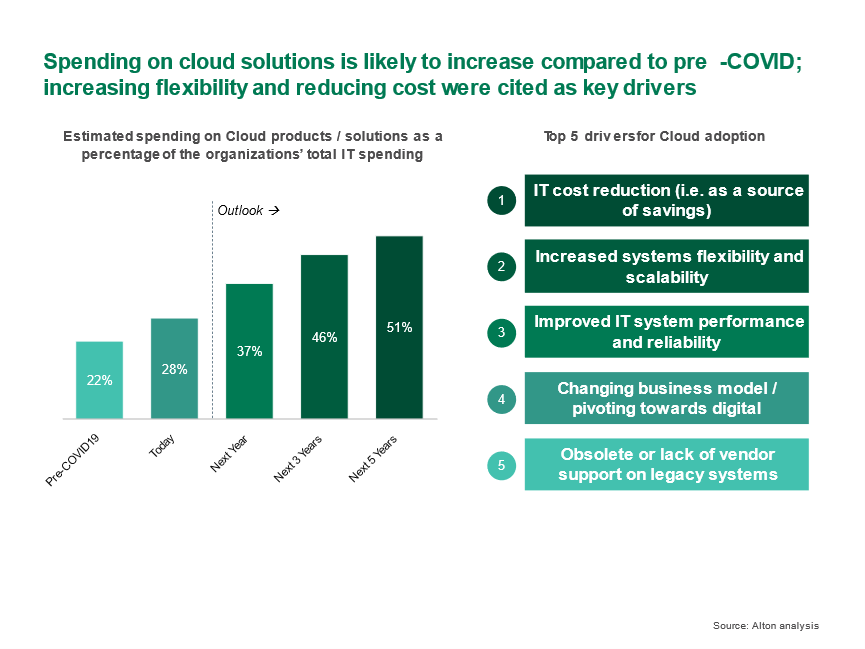

Given the flexibility, accessibility, and ease of use for Cloud services, it is also no surprise that spending on cloud products is expected to grow from 28% of total IT spending today to 51% in the next five years (figure 10), with the biggest factors driving cloud adoption cited as IT cost reductions, increased flexibility and scalability, plus improved performance and reliability.

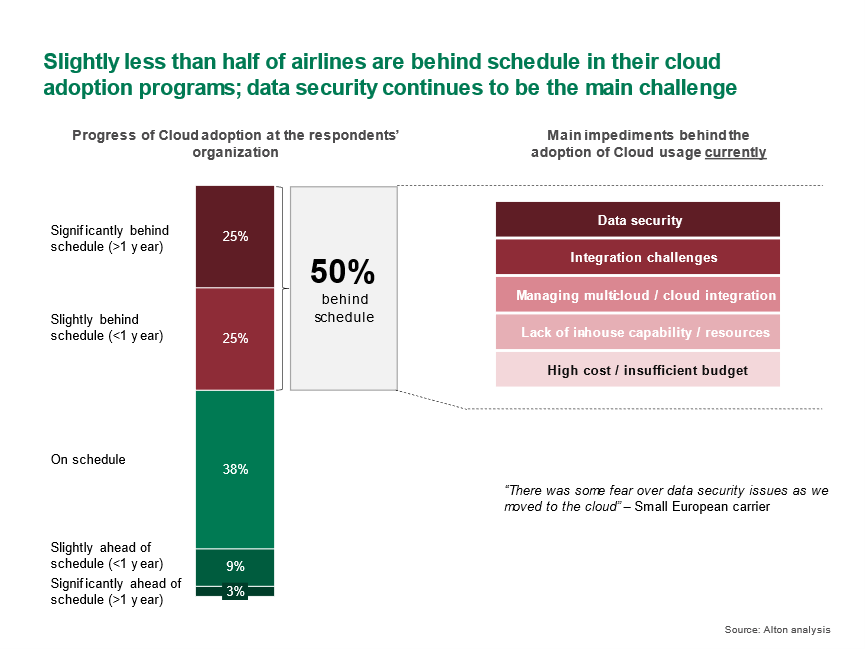

The survey asked how well respondents’ airlines were implementing their cloud adoption programs with the result that we found that half of respondents are behind schedule (figure 11).

Looking at the adoption of cloud services which looks, on the face of it, to be lagging behind the general rating of the importance of digital optimization initiatives, data security was ranked as the top impediment behind slow cloud adoption. This concern is shared across a number of areas that have been discussed in Aircraft IT in recent times and so is clearly an area that IT solution developers and vendors need to address.

Among those who indicated that cloud adoption was behind schedule, data security (see above), integration challenges, and a lack of in-house capability/resources were cited as the top stumbling blocks to implementation currently and moving into the future. That lack of in-house expertise is reflected in the finding that, when asked how they expected to achieve their IT goals, 77% of respondents expressed a preference to acquire rather than develop optimization solutions in-house, at least in the next five years. These issues were the same issues that impeded implementation in the past, indicating that they are persistent in nature and yet to be resolved.

Cybersecurity

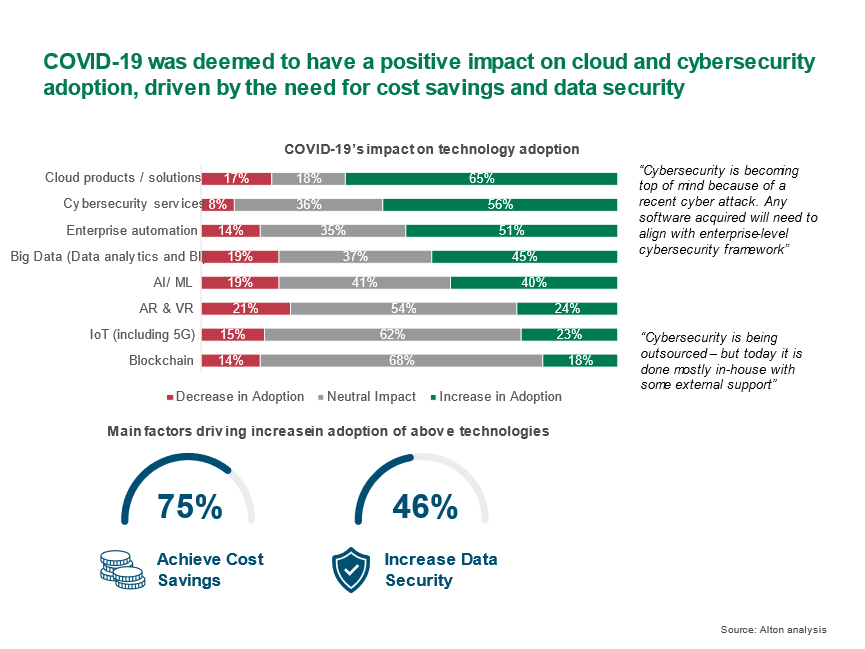

It isn’t often that we can find anything positive to say about COVID-19. However, the pandemic and how airlines had to react to it was revealed by the survey to have had a positive impact on attitudes to and prioritizing of cloud and cybersecurity adoption, driven by the need for cost savings and data security (figure 12).

COVID had the greatest impact on cloud and cybersecurity adoption being cited by 65% and 56% of respondents respectively. The most common reasons for adoption were to achieve cost savings (75% of respondents) and increase data security (46% of respondents).

Procurement considerations

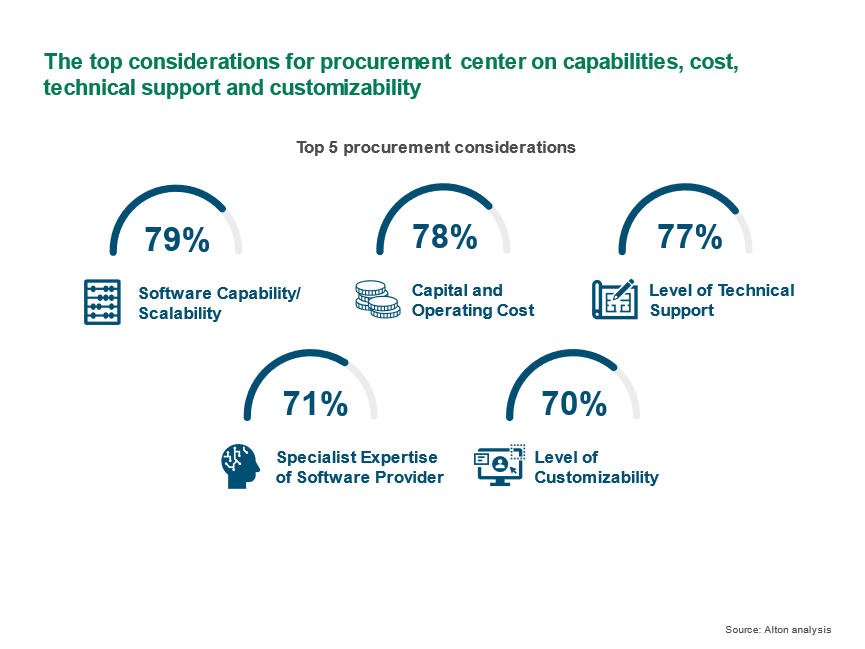

Given the responses already recorded to other questions, the top considerations for procurement decisions offer few surprises. They emphasize capabilities, cost, technical support and customizability (figure 13).

The most important procurement considerations are software capability and scalability, cited by 79% of respondents, capital and operating cost cited by 78% of respondents, and level of technical support cited by 77% of respondents. Specialist expertise, and level of customizability are also among the top procurement considerations. Notably, software brand name was ranked as significantly less important.

LOOKING TO THE FUTURE

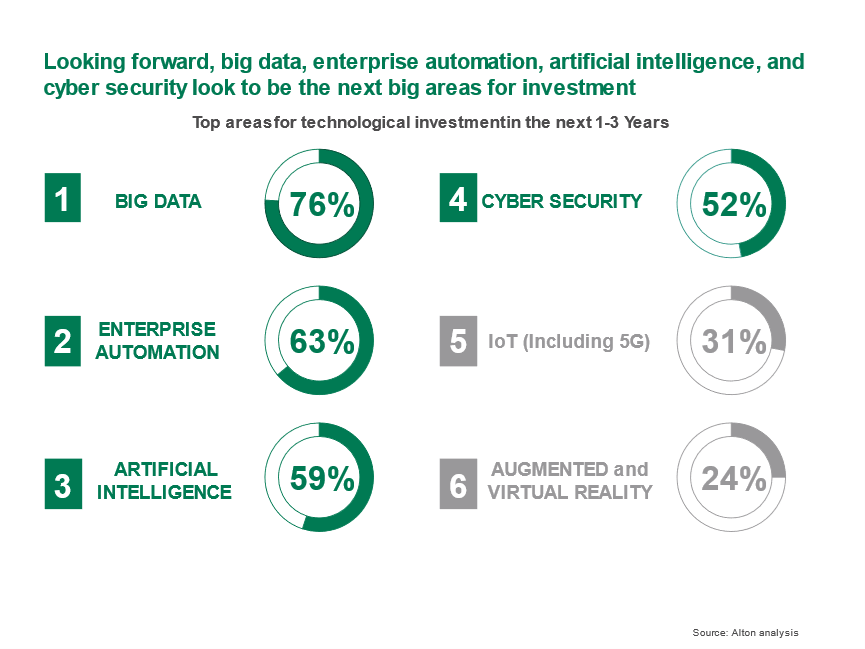

Looking forward, the majority of respondents to the survey told us that the big areas for investment over the next one to three years would be big data, enterprise automation, artificial intelligence, and cyber security (figure 14). In comparison, IoT and AR/VR technologies did not rank highly on respondents’ investment agenda in comparison.

That in itself will be of interest to solution developers and vendors given that also, 76% of respondents said that they are looking to invest in these four areas within the next one to three years. However, notwithstanding the generally heightened level of intentions regarding IT solutions, there still have to be priorities. Big data, enterprise automation, AI, and cybersecurity are the future for a majority of respondents.

SUMMARY

The COVID-19 crisis has changed aviation. For many years, we have talked about the benefits of digitalization with integrated and enhanced IT platforms for airlines, but the adoption of these new technologies has been slow. The presence of a growing volume of data available for analysis has laid the foundation for the use of analytics in aviation, however, the drive to use this data for optimization has accelerated only since the pandemic. Operators looking to reduce cost, cope with increasing operational complexities, and improve their overall competitiveness have taken the opportunity during this period to hasten their digital transformation efforts. That said, a lack of in-house expertise to implement and take advantage of the digital optimization tools creates challenges, with operators having to rely on the assistance of software providers in the near-to-medium term.

The digital transformation wave within airlines is not only centered around digital optimizers. Operators are also looking to invest in areas involving cloud technologies, Big Data, and enterprise automation. Similarly, this is driven by the need to become as cost and operationally efficient as possible, in order to build and retain a competitive edge against other airlines in an increasingly challenging industry.

[[OPEN TEXT BOX 1]]

GET THE FULL REPORT

In an article such as this, we cannot offer the type of detail that the survey generated but anyone who is interested in seeing the full report can contact Alton Aviation Consultancy and request it from Alan Lim: alan.lim@altonaviation.com

Alton Aviation Consultancy

Alton Aviation Consultancy is an independent, global aviation consulting firm with clients across commercial, financial and technical disciplines and offices in New York, Dublin, Dubai Tokyo, Beijing, Singapore, and Hong Kong. The firm has significant experience delivering large, complex consulting engagements for clients in aviation and aerospace. Alton’s global team includes seasoned industry executives from across the value chain, together with experts in business strategy, management, finance, data analysis, operations, and aerospace technology.

Comments (0)

There are currently no comments about this article.

To post a comment, please login or subscribe.